I see that if you take your SocSec at 70 you break even at roughly 80, and then it's all profit. Ten years. I grinned; if you defer your UK State Retirement Pension, after you restart there's about a ten year gap before you break even. It's too costly though; the rewards are about to be halved.

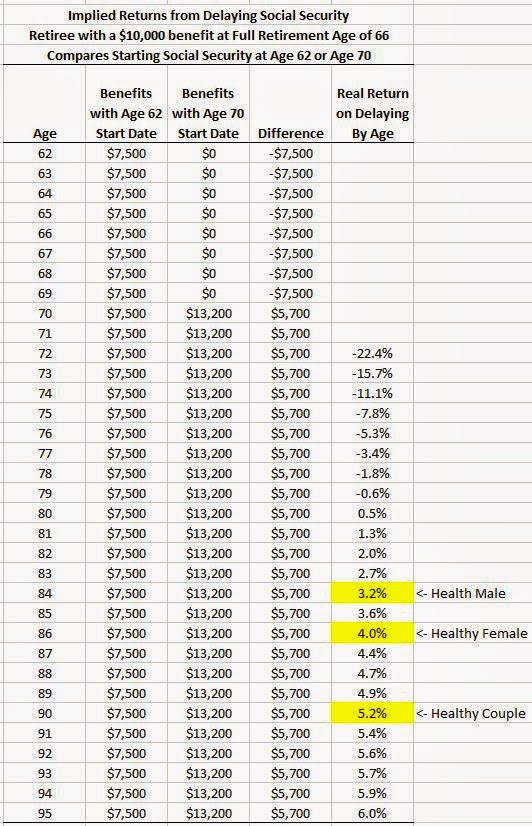

That's correct. If you add up the real value of the dollars, you would break even in the 10th year. But I don't think that should be interpreted as a long time and a negative. Retirement for a 62 year old could easily end up lasting another 25-40 years.

Does COLA apply whether you are taking the benefit or not? In the above example you may get a cola of 2% for age 63 and another 2% for age 64, etc. Does the amount you will collect at age 70 get the same COLA in the years from 62 to 70? The result would at 70 you start taking the 13,500 that has been increase by the 7 years of COLA that were applied to the age 62 example. GC

Considering that the vast majority of Americans have very little retirement savings, I suspect that the rate of people delaying Social Security will not go up. If anything, I suspect that many more people will take Social Security at 62. Moreover, I wonder what the actuarial odds of surviving are for each age level; one must be alive to enjoy the increased benefits and the analysis assumes this as fact. Perhaps if you are in good health and do not need Social Security to survive, then delaying Social security will be of some real benefit.

This is all well and good if you have a job and can postpone retirement until age 70. After 40 years of continuous employment, my employer ceased operations and I was laid off at 62. I have made up my mind that I will delay filing until full retirement age. In the meantime, I have to rely on my savings for my expenses and medical care, that used to be paid for by my employer. I'm fortunate that I started saving for retirement many years ago, but many people are in the same situation that I am and have little to no savings. I am looking for work, but the likelihood of finding anything comparable to my previous job is not promising.

I wish you the best with your search for work. It's a real problem, and it suggests a need to save even more when younger as you did. You are right, if one simply has no way to bridge the gap until 70, they may be forced to collect benefits earlier and experience a permanently lower standard of living.

That is a significant part of the problem, people near retirement age who can't work or are out of work don't have much choice other than to accept a permanently lower standard of living.

Right. If your FRA is 67, then in this example you would only get $7,000 at 62 and $12,400 at 70. Since 62 doesn't adjust to 63 and 70 to 71, this permanently reduces the amount you can get from Social Security. But it doesn't change the underlying math of when to claim. Actually, the implied return from delaying increases ever so slightly, but I think that's an artifact of the specific adjustments between ages.

Including spousal benefits of 50% FRA amount during life of working spouse, and 100% of age 70 amount at death of working spouse, makes the delay to 70 better yet.

A married couple can often further increase benefits by using the "file and suspend" strategy, whereby the head files for benefits and delays collection. The spouse collects the spousal benefit during the years where the head delays collection. The spousal benefit is not eligible to accrue delayed retirement credits in any case, so this strategy can maximize lifetime benefits for many households.

Take advantage soon though; this rule is on the chopping block as a potential means of reducing Social Security benefits for the long-term sustainability of the program.

I saw news of that. I was planning to file and suspend in my personal planning spreadsheet, but that is still 30 years off in the future. It just points out how different strategies will be, and one has to stay flexible.

A married couple can often benefit hugely - even if these "aggressive claiming procedures" are eliminated. First off, SS is really a two life annuity. As shown in the chart, that alone pushes the expected payment date out to age 90 - with a 5.2% return. But, when my wife dies at 90, I will have been in the ground for at least 3 years meaning it pays out until age 93 - for an expected 5.7% return.

I really don't get the value of break-even analysis. No healthy person knows how long they will live. If break-even were at age 68 or 92, it would be useful. But it isn't. It's around life expectancy, by design. The reason to delay SS benefits is longevity protection. If you DO live a long time, delaying will have huge benefit. If you don't live long, it won't make much difference.

There are lots of 90-year widows who wish their husband hadn't claimed early.

Most people can't afford to delay, anyway, and for them it's largely moot.

I think breakeven analysis is usually used to argue against delay. In this case, I was using it to argue in favor of delay. But indeed, Social Security is longevity insurance, and it should be thought of that way.

Actually, let me re-print an old blog post here.

---------------------------------

Kotlikoff on Social Security One follow-up point from my previous post on ESPlanner: Prof. Kotlikoff also provided a brief and clear explanation about the value of waiting to begin Social Security.

To paraphrase, one should not think about Social Security from the perspective of a breakeven investment analysis for how long it will take for Social Security pay off. That missed the point of the insurance value which Social Security provides. Using the breakeven analysis, one would not buy any insurance. On average, insurance is never expected to pay off. Insurance companies need to make a profit and cover their expenses. But the reason insurance is valuable is that it pays off in the low probability states of the world when outcomes are bad.

People cannot rely on the average outcome for their personal situation: either things work out or they don't. With Social Security, you won't feel regret by delaying Social Security and then dying before collecting benefits, because you won't be around anyway. Regret comes when you live a long life and think about how your situation would have been improved through delay. By waiting from 62 to 70 to start benefits, your benefits will be 75% larger for the rest of your life. That is a valuable safe and real annuity based on an implicit real return of 2.9%. The premiums for that annuity are the 8 years of missed Social Security benefits between 62 and 70, but all in all it can be a pretty good deal and it protects your lifestyle in the event of living a particularly long life.

The view that it's some kind of gamble (win if I live long enough, lose if I don't) is very common but I think misses a key point of delaying for the higher benefit, which is...it can increase the standard of living you can afford TODAY, right now.

How does this work? A prudent retirement plan does not assume you live to an average age. As Jim Otar puts it, that would be like building a bridge with a 50/50 chance of success. A prudent plan assumes a lifespan at least until 90 years of age...95 or even 100 is better. The financial result of assuming you will live longer can be depressing...when you run the numbers it greatly reduces how much you can afford to spend in your life, starting today and going forward. The key point is that your plan's assumption about how long you will live has a direct impact on the standard of living you can afford today.

Now consider the Social Security decision. It's very clear that if I were to live to age 90, I would "win" the bet that a delay will be good for me. If I live to less than 80, I'll "lose" the bet. The thing is, in a retirement plan, a plan that determines how much you can afford to spend today, you get to assume you will "win" that bet. That's not wishful thinking, it's a prudent assumption. It's known as claiming longevity credits, and is also key to the financial power of annuities. That longevity assumption (90+), which can be so financially cruel, works in your favor when you consider annuity type income streams. The result is that assuming a delay in taking Social Security benefits will significantly increase most families' affordable standard of living today. The closer you are to age 62, the bigger the immediate standard of living benefit.

Now you might end up "winning" or "losing" the Social Security timing bet. But in general that speculation has nothing to do with developing a prudent retirement plan and using that plan to guide your spending today.

Of course if your health or family longevity is poor, then perhaps you could justify assuming a shorter lifespan in your retirement plan, which obviously can affect the Social Security decision. For most of us though, that would not be the case.

By delaying Social Security, you can permanently increase your standard of living starting at 62 (assuming you have at least enough assets to bridge the gap). Over a long planning horizon, delaying Social Security puts a lot more resources at your disposal (high present value of lifetime benefits) and you can really take advantage of it starting immediately by spending more of your current financial assets. That's the idea of consumption smoothing from lifecycle finance.

Excellent point Grinder. It is easy to demonstrate how the SS delay will increase annual available spend by plugging the alternatives into my AAS model. Of course, inflation matters, and high inflation could reduce or negate the benefit of the delay.

I haven't seen any discussion here yet of the tax implications of delaying the start of SS benefits. The larger age-70 benefit -- possibly combined with RMD requirements from retirement accounts starting at age 70.5 -- would push some retirees into a higher tax bracket. For these individuals, the optimal age to start SS benefits may be somewhat earlier, although not necessarily as early as 62.

Every case is different, but I think that generally speaking, when you add taxes to the mix, the case for delaying Social Security is _even stronger_.

By delaying, your pre-70 income is less, which gives you more room for Roth Conversions! Roth income isn't counted when determining how much of Social Security is taxable, and if you can get a big chunk of your IRA/401(k) converted to Roth prior to 70, then you are in good shape.

How would your results look in a case where RMD's are not a factor but where a person would be in the 15% federal marginal tax bracket if SS benefits are taken starting at age 62 but all additional real $ in SS benefits from starting at age 70 instead would be taxed at a higher rate (say, 25%)?

That would delay the breakeven age in terms of after tax income, but I can't try to figure out the difference now. In this scenario, 85% of the Social Security benefit is taxable.

Here is my situation - We don't need the SS money at 62, but would still take it and use it to invest until 70 - then make withdrawals. How would this compare to SS withdrawals starting at 70.

That is essentially what this post is about. For you to be better off taking Social Security at 62 and investing it, your inflation-adjusted compounded return on your investments would have to exceed the real return shown in the table for the planning horizon you are willing to accept.

To make risks comparable, the appropriate investment would be TIPS, and I mentioned the TIPS yields in the post.

If you are thinking to instead invest the money in stocks or other risky investments, well that's up to you. I wouldn't necessarily recommend doing that because those required returns needed to beat delaying Social Security will be pretty difficult to overcome. It's not impossible, but difficult. You would need to have a pretty high risk tolerance as well as having a lot of extra discretionary wealth beyond what you need to meet your lifestyle spending goals for your strategy to be attractive.

Wade - My scenario: Delaying yearly SS of $30K at FRA until 70, for an increase of $9K per year. Can I assume that I effectively "bought" an annuity at age 70 for $120K (4yrs x $30K) that will pay me $9K per year - a return of 7.5%? Of course, the COLAs after age 70 make the return even more attractive.

Within an annuity, the 7.5% "return" per year you are referring to would include both interest and the return of principal on the $120K over time. Assuming you live to age 84 (healthy male in Wade's table), the internal rate of return on the $9K annual income stream purchased for $120K at age 70 is 0.66%. For age 86 (healthy female), the IRR would be 2.2% and for age 90 (healthy couple), the IRR would be 4.22%. That's without considering the COLA's.

James, as the previous reply notes, you are thinking about this as an annuity payout rate. This is framing the issue differently than in my table. But you can consider it your way as well.

I just checked and the best deal available right now for a CPI-adjusted SPIA for a 70-year old male has a payout rate of 5.9%.

Though there is a bit of rounding off built in to your calculation, you are describing using Social Security delay as paying $120k for a SPIA with an annual payout of $9,600. That's a payout rate of 8%, which beats commercially available annuities for single males.

With a spouse getting spousal and survivor benefits from your earnings record, the deal gets even better.

So yes, you can think about delaying Social Security as a way to buy a cheaper annuity than offered by private companies.

I guess you are correct - I haven't calculated IRR for many years. My point was to compare the $9K "extra" payment per year with the amount you would receive from a simple annuity purchased with the $120K. In today's market, you wouldn't get 7.5%. I think that is one way of looking at the decision to delay S.S.

Social security is not an investment. If it is - show me my account so that I can setup my beneficiary designations.

I guess there will never be an end to this subset of "investment porn."

Also I don't see how your spreadsheet deals with the 20% of the population that didn't even live to 62 and therefore got $0 from it? How does something like this help them?

All these writers seem to treat this situation as some sort of extra credit problem on an exam. Please.

I'm not understanding where your vitriol comes from. Would you like to see Social Security eliminated. About the under 62 deceased crowd, Social Security also provides survivor benefits for children and widows, as well as disability benefits. It's social insurance.

I support the social security system because a lot of people used it as their fall back by the time they reach the age of retirement and of course, you cannot disregard the benefits that it offers to the survivors of a member.

I see that if you take your SocSec at 70 you break even at roughly 80, and then it's all profit. Ten years. I grinned; if you defer your UK State Retirement Pension, after you restart there's about a ten year gap before you break even. It's too costly though; the rewards are about to be halved.

ReplyDeleteThat's correct. If you add up the real value of the dollars, you would break even in the 10th year. But I don't think that should be interpreted as a long time and a negative. Retirement for a 62 year old could easily end up lasting another 25-40 years.

DeleteOh yes. We've both deferred taking our UK equivalents. You betcha!

DeleteDoes COLA apply whether you are taking the benefit or not? In the above example you may get a cola of 2% for age 63 and another 2% for age 64, etc. Does the amount you will collect at age 70 get the same COLA in the years from 62 to 70? The result would at 70 you start taking the 13,500 that has been increase by the 7 years of COLA that were applied to the age 62 example. GC

ReplyDeleteGood question, and the answer is yes. You don't have to worry about this. Your initial benefit will be adjusted for the COLA even if you delay.

DeleteConsidering that the vast majority of Americans have very little retirement savings, I suspect that the rate of people delaying Social Security will not go up. If anything, I suspect that many more people will take Social Security at 62. Moreover, I wonder what the actuarial odds of surviving are for each age level; one must be alive to enjoy the increased benefits and the analysis assumes this as fact. Perhaps if you are in good health and do not need Social Security to survive, then delaying Social security will be of some real benefit.

ReplyDeleteThis is all well and good if you have a job and can postpone retirement until age 70. After 40 years of continuous employment, my employer ceased operations and I was laid off at 62. I have made up my mind that I will delay filing until full retirement age. In the meantime, I have to rely on my savings for my expenses and medical care, that used to be paid for by my employer. I'm fortunate that I started saving for retirement many years ago, but many people are in the same situation that I am and have little to no savings. I am looking for work, but the likelihood of finding anything comparable to my previous job is not promising.

ReplyDeleteBill,

DeleteI wish you the best with your search for work. It's a real problem, and it suggests a need to save even more when younger as you did. You are right, if one simply has no way to bridge the gap until 70, they may be forced to collect benefits earlier and experience a permanently lower standard of living.

That is a significant part of the problem, people near retirement age who can't work or are out of work don't have much choice other than to accept a permanently lower standard of living.

DeleteThanks,

The FRA is quickly increasing to 67. Did you run those numbers as well?

ReplyDeleteI think Wade was simply trying to show the value between 62 and 70 here, versus comparing 66/70 to 67/70.

ReplyDeleteMy reason for asking was at a 66 FRA you get 32% more by waiting, yet at a 67 FRA it is 24%.

DeleteRight. If your FRA is 67, then in this example you would only get $7,000 at 62 and $12,400 at 70. Since 62 doesn't adjust to 63 and 70 to 71, this permanently reduces the amount you can get from Social Security. But it doesn't change the underlying math of when to claim. Actually, the implied return from delaying increases ever so slightly, but I think that's an artifact of the specific adjustments between ages.

DeleteIncluding spousal benefits of 50% FRA amount during life of working spouse, and 100% of age 70 amount at death of working spouse, makes the delay to 70 better yet.

ReplyDeleteAbsolutely, strategies become more complicated for couples, and the argument in favor of one spouse delaying to 70 becomes even stronger.

DeleteA married couple can often further increase benefits by using the "file and suspend" strategy, whereby the head files for benefits and delays collection. The spouse collects the spousal benefit during the years where the head delays collection. The spousal benefit is not eligible to accrue delayed retirement credits in any case, so this strategy can maximize lifetime benefits for many households.

ReplyDeleteTake advantage soon though; this rule is on the chopping block as a potential means of reducing Social Security benefits for the long-term sustainability of the program.

I saw news of that. I was planning to file and suspend in my personal planning spreadsheet, but that is still 30 years off in the future. It just points out how different strategies will be, and one has to stay flexible.

DeleteA married couple can often benefit hugely - even if these "aggressive claiming procedures" are eliminated. First off, SS is really a two life annuity. As shown in the chart, that alone pushes the expected payment date out to age 90 - with a 5.2% return. But, when my wife dies at 90, I will have been in the ground for at least 3 years meaning it pays out until age 93 - for an expected 5.7% return.

DeleteI really don't get the value of break-even analysis. No healthy person knows how long they will live. If break-even were at age 68 or 92, it would be useful. But it isn't. It's around life expectancy, by design. The reason to delay SS benefits is longevity protection. If you DO live a long time, delaying will have huge benefit. If you don't live long, it won't make much difference.

ReplyDeleteThere are lots of 90-year widows who wish their husband hadn't claimed early.

Most people can't afford to delay, anyway, and for them it's largely moot.

Dirk,

DeleteI think breakeven analysis is usually used to argue against delay. In this case, I was using it to argue in favor of delay. But indeed, Social Security is longevity insurance, and it should be thought of that way.

Actually, let me re-print an old blog post here.

---------------------------------

Kotlikoff on Social Security

One follow-up point from my previous post on ESPlanner: Prof. Kotlikoff also provided a brief and clear explanation about the value of waiting to begin Social Security.

To paraphrase, one should not think about Social Security from the perspective of a breakeven investment analysis for how long it will take for Social Security pay off. That missed the point of the insurance value which Social Security provides. Using the breakeven analysis, one would not buy any insurance. On average, insurance is never expected to pay off. Insurance companies need to make a profit and cover their expenses. But the reason insurance is valuable is that it pays off in the low probability states of the world when outcomes are bad.

People cannot rely on the average outcome for their personal situation: either things work out or they don't. With Social Security, you won't feel regret by delaying Social Security and then dying before collecting benefits, because you won't be around anyway. Regret comes when you live a long life and think about how your situation would have been improved through delay. By waiting from 62 to 70 to start benefits, your benefits will be 75% larger for the rest of your life. That is a valuable safe and real annuity based on an implicit real return of 2.9%. The premiums for that annuity are the 8 years of missed Social Security benefits between 62 and 70, but all in all it can be a pretty good deal and it protects your lifestyle in the event of living a particularly long life.

The view that it's some kind of gamble (win if I live long enough, lose if I don't) is very common but I think misses a key point of delaying for the higher benefit, which is...it can increase the standard of living you can afford TODAY, right now.

ReplyDeleteHow does this work? A prudent retirement plan does not assume you live to an average age. As Jim Otar puts it, that would be like building a bridge with a 50/50 chance of success. A prudent plan assumes a lifespan at least until 90 years of age...95 or even 100 is better. The financial result of assuming you will live longer can be depressing...when you run the numbers it greatly reduces how much you can afford to spend in your life, starting today and going forward. The key point is that your plan's assumption about how long you will live has a direct impact on the standard of living you can afford today.

Now consider the Social Security decision. It's very clear that if I were to live to age 90, I would "win" the bet that a delay will be good for me. If I live to less than 80, I'll "lose" the bet. The thing is, in a retirement plan, a plan that determines how much you can afford to spend today, you get to assume you will "win" that bet. That's not wishful thinking, it's a prudent assumption. It's known as claiming longevity credits, and is also key to the financial power of annuities. That longevity assumption (90+), which can be so financially cruel, works in your favor when you consider annuity type income streams. The result is that assuming a delay in taking Social Security benefits will significantly increase most families' affordable standard of living today. The closer you are to age 62, the bigger the immediate standard of living benefit.

Now you might end up "winning" or "losing" the Social Security timing bet. But in general that speculation has nothing to do with developing a prudent retirement plan and using that plan to guide your spending today.

Of course if your health or family longevity is poor, then perhaps you could justify assuming a shorter lifespan in your retirement plan, which obviously can affect the Social Security decision. For most of us though, that would not be the case.

Absolutely!

DeleteBy delaying Social Security, you can permanently increase your standard of living starting at 62 (assuming you have at least enough assets to bridge the gap). Over a long planning horizon, delaying Social Security puts a lot more resources at your disposal (high present value of lifetime benefits) and you can really take advantage of it starting immediately by spending more of your current financial assets. That's the idea of consumption smoothing from lifecycle finance.

Excellent point Grinder. It is easy to demonstrate how the SS delay will increase annual available spend by plugging the alternatives into my AAS model. Of course, inflation matters, and high inflation could reduce or negate the benefit of the delay.

DeleteWell put Grinder, thank you.

DeleteI haven't seen any discussion here yet of the tax implications of delaying the start of SS benefits. The larger age-70 benefit -- possibly combined with RMD requirements from retirement accounts starting at age 70.5 -- would push some retirees into a higher tax bracket. For these individuals, the optimal age to start SS benefits may be somewhat earlier, although not necessarily as early as 62.

ReplyDeleteEvery case is different, but I think that generally speaking, when you add taxes to the mix, the case for delaying Social Security is _even stronger_.

DeleteBy delaying, your pre-70 income is less, which gives you more room for Roth Conversions! Roth income isn't counted when determining how much of Social Security is taxable, and if you can get a big chunk of your IRA/401(k) converted to Roth prior to 70, then you are in good shape.

How would your results look in a case where RMD's are not a factor but where a person would be in the 15% federal marginal tax bracket if SS benefits are taken starting at age 62 but all additional real $ in SS benefits from starting at age 70 instead would be taxed at a higher rate (say, 25%)?

DeleteThat would delay the breakeven age in terms of after tax income, but I can't try to figure out the difference now. In this scenario, 85% of the Social Security benefit is taxable.

Deleteits very helpful post and good article for all user. We should read it again and and again. You can see more

ReplyDelete12 Month Payday Loans, Text Loans

Here is my situation - We don't need the SS money at 62, but would still take it and use it to invest until 70 - then make withdrawals. How would this compare to SS withdrawals starting at 70.

ReplyDeleteThat is essentially what this post is about. For you to be better off taking Social Security at 62 and investing it, your inflation-adjusted compounded return on your investments would have to exceed the real return shown in the table for the planning horizon you are willing to accept.

DeleteTo make risks comparable, the appropriate investment would be TIPS, and I mentioned the TIPS yields in the post.

If you are thinking to instead invest the money in stocks or other risky investments, well that's up to you. I wouldn't necessarily recommend doing that because those required returns needed to beat delaying Social Security will be pretty difficult to overcome. It's not impossible, but difficult. You would need to have a pretty high risk tolerance as well as having a lot of extra discretionary wealth beyond what you need to meet your lifestyle spending goals for your strategy to be attractive.

Wade - My scenario: Delaying yearly SS of $30K at FRA until 70, for an increase of $9K per year. Can I assume that I effectively "bought" an annuity at age 70 for $120K (4yrs x $30K) that will pay me $9K per year - a return of 7.5%? Of course, the COLAs after age 70 make the return even more attractive.

ReplyDeleteWithin an annuity, the 7.5% "return" per year you are referring to would include both interest and the return of principal on the $120K over time. Assuming you live to age 84 (healthy male in Wade's table), the internal rate of return on the $9K annual income stream purchased for $120K at age 70 is 0.66%. For age 86 (healthy female), the IRR would be 2.2% and for age 90 (healthy couple), the IRR would be 4.22%. That's without considering the COLA's.

DeleteJames, as the previous reply notes, you are thinking about this as an annuity payout rate. This is framing the issue differently than in my table. But you can consider it your way as well.

DeleteI just checked and the best deal available right now for a CPI-adjusted SPIA for a 70-year old male has a payout rate of 5.9%.

Though there is a bit of rounding off built in to your calculation, you are describing using Social Security delay as paying $120k for a SPIA with an annual payout of $9,600. That's a payout rate of 8%, which beats commercially available annuities for single males.

With a spouse getting spousal and survivor benefits from your earnings record, the deal gets even better.

So yes, you can think about delaying Social Security as a way to buy a cheaper annuity than offered by private companies.

I guess you are correct - I haven't calculated IRR for many years. My point was to compare the $9K "extra" payment per year with the amount you would receive from a simple annuity purchased with the $120K. In today's market, you wouldn't get 7.5%. I think that is one way of looking at the decision to delay S.S.

ReplyDeleteSocial security is not an investment. If it is - show me my account so that I can setup my beneficiary designations.

ReplyDeleteI guess there will never be an end to this subset of "investment porn."

Also I don't see how your spreadsheet deals with the 20% of the population that didn't even live to 62 and therefore got $0 from it? How does something like this help them?

All these writers seem to treat this situation as some sort of extra credit problem on an exam. Please.

I'm not understanding where your vitriol comes from. Would you like to see Social Security eliminated. About the under 62 deceased crowd, Social Security also provides survivor benefits for children and widows, as well as disability benefits. It's social insurance.

DeleteI support the social security system because a lot of people used it as their fall back by the time they reach the age of retirement and of course, you cannot disregard the benefits that it offers to the survivors of a member.

ReplyDelete